A Guest Post by Voisard Asset Management Group

Charitable bequests are a great way to satisfy both personal and financial planning goals. If charitable giving is a priority within your financial plan, we have good news! U.S. tax code is designed to encourage charitable gifts. Given various charitable gifting options available, it is important to determine the most appropriate and efficient way to pass assets to designated entities.

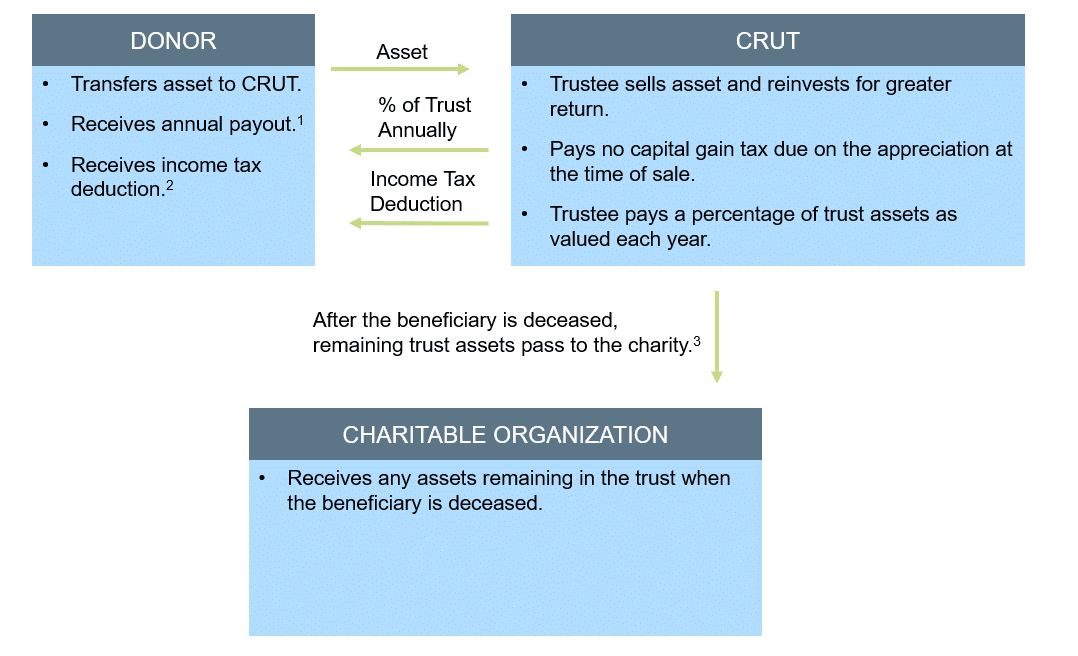

So, what is a Charitable Remainder Trust? A Charitable Remainder Unitrust (CRUT) is one way to gift assets and receive tax benefits in the year of the gift while still being able to access a portion of the funds. Assets placed in a CRUT are irrevocable, have current income tax advantages and may pay an annual fixed percentage of the balance (5-50%) to one or more beneficiaries. The remaining balance of assets within the CRUT are passed to the charitable entity after the death of the beneficiaries. Beneficiaries can be the donor of the trust assets, donor’s spouse, children, or anyone the grantor wishes to designate. This strategy allows the donor to retain their rights to a fixed percentage of the annual trust assets based on the annual year-end balance. There is also an IRS requirement that the charitable gift must be at least 10% of the fair market value of the assets at the time of contribution to the CRUT.

One appeal to the CRUT strategy is that the charitable deduction is typically given in the current year. If the gifted amount exceeds the allowed percentage of the donor’s annual earnings, excess deductions may be carried over into future years. Another benefit of utilizing a CRUT is that highly appreciated assets can be transferred into the trust, potentially avoiding capital gains tax for the donor. Once transferred, the trustee can sell assets within the trust without paying capital gains tax and reinvest the proceeds into other assets. This allows for the potential of increased cash-flow (taxable to the recipient as income) for the beneficiaries. Because the trust is established with a set pay-out rate, it can be set up to produce cash payments that were higher than the previously realized rate of return. This, coupled with tax advantages, can provide a substantial increase in the donor’s cash flows.

When applied to business owners’ circumstances, a CRUT is a planning vehicle that is often underutilized. When properly implemented, a CRUT can help mitigate capital gain tax liability, create a charitable legacy, supplement retirement income, receive a significant income tax deduction, and reduce estate taxes. Additionally, it can be utilized to transfer ownership proceeds of the family business to a younger generation. When used as part of an exit plan, the highly-appreciated C corp stock (and/or real estate) is placed within the trust. The trust is tax-exempt and can sell these appreciated assets without triggering capital gain taxation. Once in place, the CRUT sells your ownership interest to an outside buyer and the proceeds become an income stream in retirement (less the 10% that is required to go to the designated charity or non-profit). This benefit, along with the charitable tax deduction, can prove to be very powerful when implemented properly. (Please note, S corp stock is not eligible. A CRUT would cause the company to lose its S corp status.)

When looking to sell your company, it is important that you have a team of trusted financial planning advisors, tax advisors, legal counsel, and business advisors work cohesively to efficiently help you reach your financial goals. If you would like to learn if a Charitable Remainder Trust is an option for you, please contact Voisard Asset Management at (616) 988-5778.

Voisard Asset Management Group is a full-service financial planning and wealth management firm that assists clients with creating individualized financial plans. Our team of professionals include Certified Financial Planning® professionals all capable of walking you through this process. Our website can be found at www.voisardgroup.com.