“Patience, persistence and perspiration make an unbeatable combination for success.” – Napoleon Hill

When many business owners hear the word auction, they immediately think of distress, liquidation, and hard times. The term often evokes memories of the Great Recession, the uncertainty of the COVID-19 shutdowns, or situations where struggling companies were forced to sell machinery, inventory, office furniture, and other assets to the highest bidder simply to survive.

But not all auctions are created equally.

In the world of mergers and acquisitions, a limited auction process is a strategic and highly effective method for maximizing value when selling a business. Rather than auctioning off assets, a limited auction involves inviting a select group of qualified buyers to confidentially evaluate and compete for the acquisition of a company. After being given sufficient time to review information, meet with management, and understand the opportunity, interested buyers are asked to submit their best offers within a structured process.

At Calder Capital, we believe that when executed properly, a limited auction process can be one of the most powerful tools available to business owners. For companies with the right characteristics, it helps ensure that no value is left on the table while moving the transaction forward as efficiently as market conditions allow.

Our experience as a sell-side M&A advisor has consistently demonstrated that a well-run limited auction process produces three critical benefits: higher valuations, stronger deal terms, and greater transaction certainty. By creating a competitive environment among qualified buyers, sellers gain leverage throughout negotiations, reduce dependence on any single bidder, and often achieve outcomes that would not have been possible through one-on-one negotiations alone.

Why Are We Writing About Limited Auction Processes?

There are two primary reasons we are sharing our insights on the Limited Auction Process:

First, we are passionate about helping business owners achieve both the best outcome and the best experience.

Our goal is not only to maximize purchase price and deal terms, but also to ensure that business owners have a positive, well-managed sale process. Unfortunately, many business brokers, investment bankers, and M&A advisors fail to fully educate their clients on the benefits of creating a competitive, limited auction environment. As a result, owners may unknowingly leave value on the table or endure a more difficult transaction than necessary.

Secondly, we believe there is a common misconception about the value brokers, bankers, and advisors bring to a transaction.

Many firms are hired because they claim to “know buyers.” While relationships certainly matter, rarely does an advisor know in advance which specific buyer will ultimately acquire a company. The true value lies not in having a list of buyers, but in knowing how to run an effective sale process that attracts the right buyers, creates competition, and drives stronger outcomes. In our experience, a well-executed limited auction process is far more important than any individual buyer relationship because the process itself is what generates interest, leverage, and ultimately, superior results.

What Types of Businesses Work Well for Limited Auction Style Sales?

Not every company possesses the characteristics necessary to maximize the benefits of competitive bidding.

The most important characteristic of a business that is well-suited for a limited auction process is low owner dependency. We have documented examples here of how this factor contributed to successful business sales.

If the owner remains heavily involved in the day-to-day operations of the company and lacks a clear exit strategy beyond finding a replacement through the sale process, generating competitive bids becomes more challenging. Most buyers are not looking to simply “buy a job.” Rather, they are seeking to acquire an investment, an asset that can continue to grow, generate returns, and ultimately be sold for a profit in the future.

While it is certainly possible to receive multiple offers for an owner-dependent business, negotiating leverage is often reduced. Buyers are generally less willing to pay premium valuations for a company whose success depends largely on a single individual. Push too hard in negotiations, and buyers may simply walk away from the table.

The second characteristic of a business that is well-positioned for a limited auction process is strong cash flow.

While there are no definitive studies identifying the precise level of cash flow required to create a truly competitive auction environment, our experience indicates that companies generating approximately $500,000 or more in Seller’s Discretionary Earnings (SDE) or EBITDA tend to attract significant buyer interest when marketed properly. At that level, the business typically generates enough cash flow to provide the buyer with a market-rate salary while still supporting debt service and future investment in the company.

For strategic buyers, an owner can often be replaced by a professional manager earning between $75,000 and $150,000 annually, leaving substantial cash flow available to support the acquisition. When a business cash flows $750,000+, the real competition begins. At that level, lower-middle-market private equity firms often join strategic buyers and high-net-worth individuals in pursuing the opportunity.

Max Friar, Founder and Managing Partner of Calder Capital, states, “When we can get individuals, strategic buyers, and private equity groups interested in the same company at the same time, a perfect storm is brewing for our clients.”

What are the stages of a Limited Auction Style Business Sale?

Pre-Market Stage

A successful limited auction process begins with developing a thorough understanding of the company, including its operations, value drivers, growth opportunities, marketability, and areas where a buyer may be able to create additional value.

The findings from this analysis are compiled into a Confidential Information Memorandum (CIM), a professional marketing document that provides qualified buyers with a comprehensive overview of the business after they have executed a Non-Disclosure Agreement (NDA).

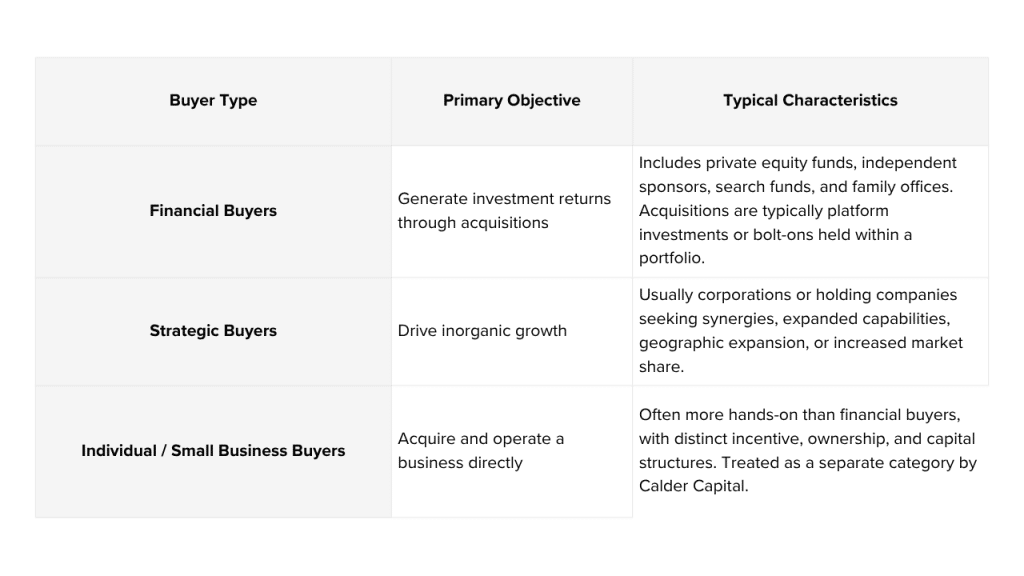

This pre-market stage is where much of the heavy lifting occurs. While financial analysis is being completed and the CIM is being prepared, a simultaneous research effort is underway to identify potential strategic, financial, and entrepreneurial buyers. Learn more about buyer types in the table below.

Qualified buyers can be sourced from a variety of channels. The key is conducting thorough research, or, in our case, maintaining a comprehensive database of prospective acquirers that includes business owners, CEOs, presidents, private equity professionals, and other active buyers, along with their contact information and acquisition criteria.

Once the business is ready to go to market, these buyers are contacted through targeted outreach efforts, including phone calls and email campaigns. At the same time, the opportunity is marketed through major M&A listing platforms and distributed to the advisor’s network of buyers, investors, lenders, and referral partners to maximize visibility and generate interest.

Going-To-Market

If the business has desirable characteristics, particularly strong cash flow and limited owner dependency, the first two to three weeks of marketing can be very active. When working with Calder Capital, it is not uncommon for more than 100 qualified buyers to express interest during this initial period.

This stage requires significant time spent communicating with prospective buyers, answering questions, and vetting them on behalf of the client. After the business officially goes to market, a funnel begins to take shape. Marketing efforts may reach thousands of potential buyers. From there, perhaps 100 will inquire. Some will not be financially qualified. Others will drop out after reviewing the opportunity more closely or determining that it is not the right fit.

The remaining group of serious, qualified buyers will then move into a deeper review process. At this stage, they may ask detailed questions, schedule management calls or site visits, and begin more substantive conversations with the business owner and the owner’s M&A advisor.

Accepting and Evaluating Offers

Once our client and our team are confident that sufficient buyer interest exists, it is time to establish a deadline for offers. Timing is critical. Buyers need enough time to become familiar with the business and gain comfort with the opportunity, but not so much time that the process loses momentum.

Given unlimited time, many buyers will attempt to conduct the majority of their due diligence before submitting an offer. When there are ten or more legitimate buyers interested in making an initial proposal, we typically establish a firm offer deadline. Doing so forces serious buyers to act in unison and encourages them to put their best foot forward if they truly want to acquire the company.

Let’s assume the process results in eight offers. Upon receipt, it is essential to carefully review each proposal, ask clarifying questions, and create a net proceeds comparison so the seller can quickly understand the true economic impact of each offer.

While buyers submit formal Indications of Interest (IOIs) and, later, Letters of Intent (LOIs), the language and structure of these documents can be difficult for sellers to interpret. At Calder Capital, we provide our clients with clear summaries and side-by-side comparisons that translate complex deal terms into understandable outcomes, allowing them to make informed decisions with confidence.

With multiple offers in hand, it is common for several to be eliminated immediately. Despite a competitive process, many buyers will still submit low or average offers. Some assume the competition is not real, while others simply fail to recognize that winning a desirable business often requires paying a premium.

As Friar notes, “It is amazing how often buyers are shocked when their offer is rejected. There can be a tendency among some buyers to think they are the best thing since sliced bread simply because they are qualified to acquire a company. There is nothing more humbling in mergers and acquisitions than a well-run limited auction process.”

One of the most beneficial aspects of the LOI stage is that the most sophisticated buyers often rise to the top. They understand the process, have the capital to complete the transaction, present themselves professionally, and communicate a thoughtful vision for the future of the business. That preparation and professionalism frequently give sellers confidence that they are choosing the right buyer, not just the highest bidder.

Due Diligence and Negotiations

Once a Letter of Intent has been executed, the transaction moves into due diligence. While this stage presents its own challenges, it is also where one of the greatest advantages of a limited auction process becomes apparent.

When multiple qualified buyers remain interested in the business, sellers gain significant negotiating leverage should the selected buyer attempt to reduce the purchase price or weaken the deal terms during due diligence. Buyers know that attractive acquisition opportunities are scarce, and the presence of alternative interested parties can help keep negotiations balanced and productive.

Friar recalls one such transaction, “In one of my earlier deals, a buyer became concerned during an extended due diligence period that my client’s sales were not as strong as they were upon going to market. As a result, the buyer proposed changing $500,000 of the purchase price, approximately 20% of the deal, from cash at closing into an earnout. Since we had already signed an LOI based on a full-cash offer, the seller was understandably disappointed by the proposed change, even though the concerns about his company’s sales were legitimate.”

Fortunately, there was still meaningful interest from other buyers. Without making threats or creating unnecessary conflict, we reminded the buyer that other options existed and that returning to the market remained a possibility. We also allowed the buyer time to reconsider his position. Ultimately, the parties reached a compromise: only $150,000 was converted to an earnout, while $350,000 of that $500,000 portion remained payable in cash at closing.”

This example illustrates why maintaining competitive tension throughout the sale process is so important. Even after an LOI is signed, having credible alternative buyers can help sellers preserve value, negotiate from a position of strength, and avoid unnecessary concessions during one of the most critical stages of the transaction.

Limited Auction Sales Processes, in Summary

A limited-auction style sale keeps the power in the hands of the seller the entire time. And if you’re selling your company and relying on the proceeds for retirement, college savings, and your family’s future security.

Across the hundreds of sell-side transactions Calder Capital has completed, the vast majority have followed a limited auction-style sale process. In our experience, this approach consistently helps sellers achieve stronger pricing, better terms, and greater transaction certainty.

By creating subtle, professional competition among qualified buyers, a limited auction process encourages serious buyers to put their best offers forward. It also provides valuable protection during due diligence, helping reduce the risk of unnecessary re-trading (aggressive re-negotiation of offer terms), excessive nitpicking, or attempts to weaken the agreed-upon deal structure.

Most importantly, a limited auction process helps keep leverage where it belongs: in the hands of the seller. For many business owners, the proceeds from a sale are a meaningful element of their retirement security, kids’ or grandkids’ college savings, generational wealth, and it will greatly influence the financial future of their family. When the stakes are that high, sellers should be intentional about preserving as much negotiating power as possible.

After all, if you are selling your company, why give buyers any more leverage than absolutely necessary?

About Calder Capital:

Founded in 2013, Calder Capital is a cross-industry mergers and acquisitions advisory firm with offices across the United States. Calder provides valuation, sell-side, and buy-side services. We are nationally recognized for excellence in advising $1-100M enterprise value transactions in manufacturing, construction, distribution, and business services. Calder serves business owners, entrepreneurs, family offices, financial buyers, and investors. Learn more at www.CalderGR.com.

Notice: Calder Capital, LLC is not affiliated with any similarly named organizations or entities. To verify communications from our firm, visit our website or contact [email protected].